Meta Plunges After Boosting Capex Outlook Again On “Higher Component Pricing”

The last of the giga-caps to report today, the increasingly more misnamed Meta Platforms, had some good news to report for the just completed Q1. It also had bad news, and judging by the plunge in the stock price, the market is focusing on the latter.

First, the good news: the company reported revenue and EPS both of which beat estimates, and guided Q2 revenues which came in roughly in line with estimates. Here is the breakdown.

- EPS $10.44 vs. $6.43 y/y, and beating estimates of $6.66; one note: the EPS print included a $8.03BN income tax benefit recognized in the first quarter of 2026. Excluding this benefit, EPS would have been $3.13 lower or $7.31 (at a 37 effective tax rate)

Revenue was also solid across the board

- Revenue $56.31 billion, +33% y/y, beating estimate $55.51 billion

- Advertising rev. $55.02 billion, +33% y/y, beating estimate $54.16 billion

- Family of Apps revenue $55.91 billion, +33% y/y, beating estimate $55 billion

- Reality Labs revenue $402 million, -2.4% y/y, missing estimate $508 million

- Other revenue $885 million, +74% y/y, beating estimate $741.4 million

Going down the line:

- Operating income $22.87 billion, +30% y/y

- Operating margin 41% vs. 41% y/y

Broken down by segment:

- Family of Apps operating income $26.90 billion, +24% y/y, beating estimate $24.26 billion

- Reality Labs operating loss $4.03 billion vs. loss $4.21 billion y/y, vs estimate loss $4.77 billion

Ad impressions were more mixed with ad impressions beating, Avg price per ad in line, and Avg family service users per day missing

- Ad impressions +19% vs. +5% y/y, beating estimate +16.2%

- Average price per ad +12% vs. +10% y/y, in line estimate +12%

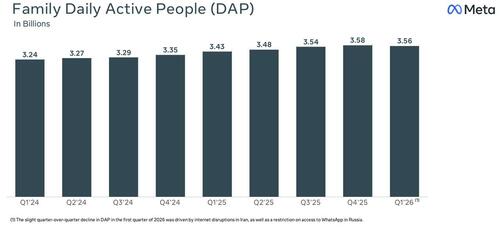

- Average Family service users per day 3.56 billion, +3.8% y/y, missing estimate 3.61 billion

The last one is a problem because as shown below, this is the first drop in the company’s DAP in years.

Looking ahead, the guidance was also solid with a modest increase in Q2 revenue:

- Meta sees revenue $58 billion to $61 billion, in line with the estimate $59.56 billion

- Meta still sees total expenses $162 billion to $169 billion, also in line with estimate $164.6 billion

That was the good news. The bad news, as a quarter ago when the company was slammed for its massive increase in forecast capex spending, had everything to do with – what else – capex.

Just like last quarter, Meta raised its capex outlook for the year, again, extending its streak of plowing historic levels of investment into the race to build ever-advancing artificial intelligence systems.

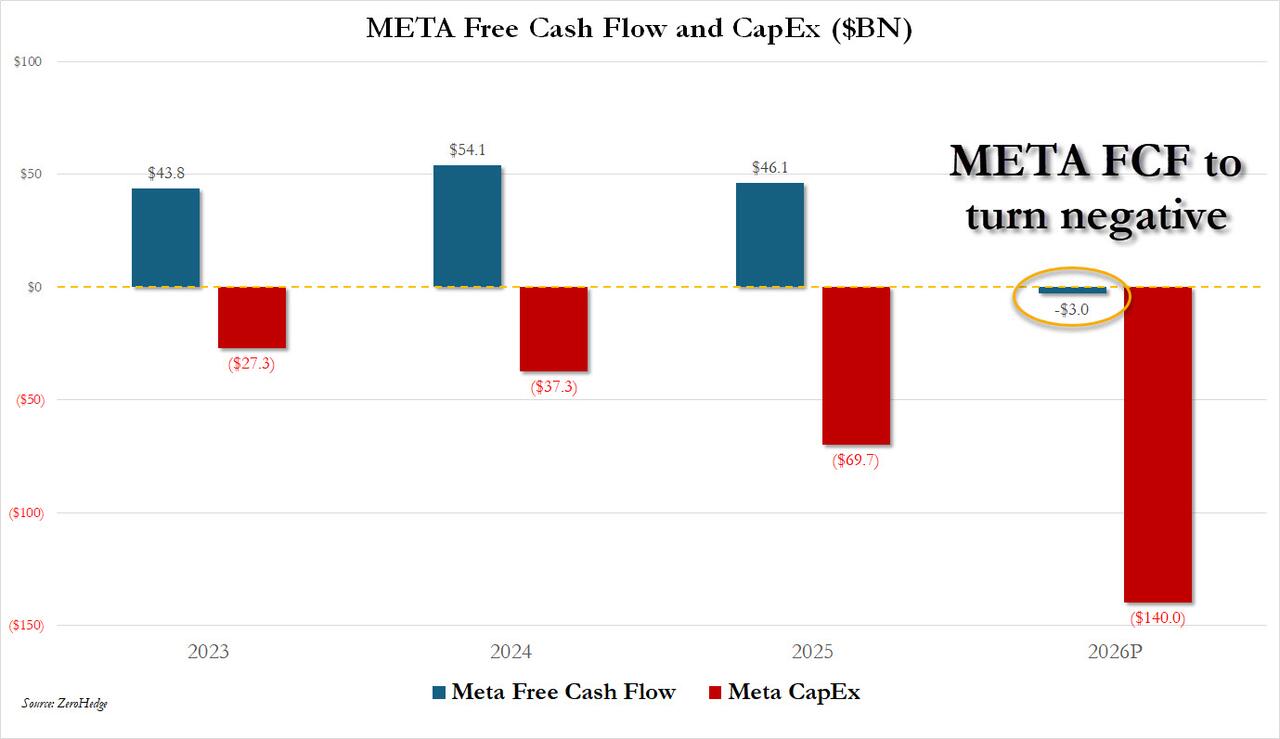

The social-media giant projected full-year capital expenditures between $125 billion and $145 billion, far exceeding analysts’ estimates and marking a roughly 7.4% increase from the $115-$135 billion range the company had previously projected. The company is dealing with “higher component pricing” and additional data center costs”, CFO Susan Li said in a statement. At this rate, which has seen the company raise its capex by $10BN every 3 months, the company’s Free Cash Flow will be deeply negative soon.

And as capex soars without a corresponding increase in revenue/EBITDA, the company’s Free Cash Flow is now set to turn negative in 2026.

To offset its AI spending, Meta has recently imposed a number of cost-cutting measures. Last week, it alerted staff in an internal memo that it would be cutting roughly 8,000 jobs and wouldn’t be filling 6,000 open roles. The company had already carried out other, more limited cuts earlier this year that hit its hardware division Reality Labs, among other teams.

Evercore ISI estimated the May layoffs will save the company about $3 billion annually, and that companies will rely more on AI agents to help do tasks that once required human employees. “We believe the industry is just beginning to realize the growth opportunities coming out of agentic deployments – and the stepped-up level of investments required to support them,” Evercore analyst Mark Mahaney said in a note to investors.

Meta CEO Mark Zuckerberg had already signaled that his company will spend hundreds of billions of dollars on AI infrastructure before the end of the decade. And that was before a memory chip shortage triggered a surge in prices. The firm has announced billion-dollar deals with Nvidia Corp., Advanced Micro Devices Inc. and Broadcom Inc. for chips and other hardware and is building several massive data centers to power its efforts.

The silver lining is that there are some early signs that Meta’s investments in AI are beginning to pay off. Earlier in April, Meta debuted its latest artificial intelligence model, Muse Spark — the first released since Zuckerberg embarked on a multibillion-dollar overhaul of the company’s AI organization last year. Additional large language models are expected to roll out later this year.

The company is also facing its various legacy risks: Meta faces a threat from mounting child safety litigation. In a landmark ruling in March, a jury found Meta liable for a 20-year-old woman’s mental health struggles, which she said were caused by her addiction to social media. While Meta must pay millions to the plaintiff, the ruling could expose the company to billions of dollars in risk from additional lawsuits. Two other bellwether cases are scheduled to go to trial in California state court later this year. Meta acknowledged on Wednesday that it continues to “see scrutiny on youth-related issues and have additional trials scheduled for this year in the U.S., which may ultimately result in a material loss.”

While Meta’s stock rallied following Muse Spark’s unveiling, wiping out prior losses, it tumbled after the market was less than happy with the yet another capex increase which has yet to show tangible returns on the top line. META plunged as much as 6%, sending its stock back to red for the year.

Tyler Durden

Wed, 04/29/2026 – 17:14

Google Search